There's so much information on this page. To learn how you can make every day feel like a Saturday and have option to fire your boss, click on the button above. To learn more about our coaching programs to safely invest in Real Estate, click on the button above.

Below you will find a ton of info. Take your time. If you find yourself getting overwhelmed, take a break. Or better yet, contact us to find out how we can help. Real Estate is FUN and EASY.

New content is always being added, so sign up to get notified when new content is added. (Go to the very bottom)

Get Complimentary Access to the ON-LINE Mortgage-Free video course on the Academy.

Click here (No credit card required)

Learn about the GLAD method, which is available to everyone with a mortgage at no extra cost. Also learn

- how you can turn your mortgage into a tax deduction

- how to save thousands in interest cost

- how to pay off your mortgage in under 10 years (or any other debt)

- and more

RRSP Withdrawel to pay off debt. STOP. Get a 2nd option

Stuff happens in life and sometimes, we find we go into debt. An option would be to withdraw funds from our RRSP to help pay off some debt.

Stop. Wait.

Before you take money out of your RRSP, watch this video. There are a few things to consider. And there may be another option.

Myth 1: It's Too Much Work

You know whats more work then becoming mortgage-free?

Having to work past the age of 65, living pay-cheque-to-pay-cheque...

Here is 1 common Myth about becoming Mortgage-Free

Have you ever said this: Its too much work, I have to sacrifice too much...

Learn ways you can save money each month.

Learn how to still travel and pay your mortgage off in 10 years.

Negative Cashflow May Be a Good Idea

Contrary to most education programs on Real Estate that says to buy positive cash flow properties, Michel LaFleur shares 2 scenario when it may make sense to buy negative cash flow properties. This strategy is for seasoned/creative investors and not recommended for newbie investors.

To watch the video click here.

Negative cash flow is when you have to pay out of your own pocket each month. After all expenses including mortgage, insurances, taxes, etc. Many teach that Cashflow is KING. Cashflow is 1 of many factors to look at when buying a property. Learn when negative cashflow may be a good idea. It could take you to the next level of being a real estate investor.

Here is a breakdown of what you will hear:

20:35 Scenario 1: Negative Cash Flow Makes Sense

28:32 Scenario 2: Negative Cash Flow Makes Sense

37:28 You will pay 1.5 X more in interest for your property if you have a mortgage

38:50 Distress property

44:16 Rapid Cash / AFS (Agreement for Sale)

49:53 Rent-to-own (No-More-Rent), Lease Option

52:54 Negative Cash Flow info

To watch the video and get access to other videos/tools/reports all for free click here.

Avoid Landlord Mistakes

For all property owners and property managers, this information is critical in your tenant toolbox to helping you ensure you screen the right tenants. No one wants a bad tenant. This is how to

ensure you protect your assets.

Get the free report on the top 5 critical mistakes made by Landlords. Get access to the training course.

To watch the video click here.

Although this workshop is no longer available, you can watch the recording (click here).

Also, get Complimentary Access to the ON-LINE Mortgage-Free video course on the Academy.

Click here and set up a profile (No credit card required)

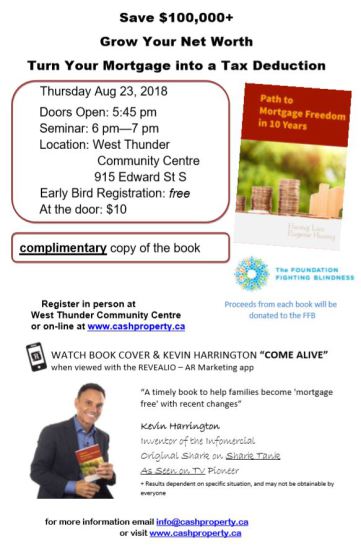

** Book Release **

Read this book to find out how you can pay off your mortgage in 10 years.

You’ll be GLAD you did!

Home ownership is one of the great privileges that Canadians have. In recent years, with such low mortgage interest rates compared to the late 1990's, many families have taken on a mortgage that they don't know how to pay off. Can you believe that one in every four Canadian homeowners between the ages of 60 and 69 still has a mortgage?

Many of our coaching clients express concerns about how their children will ever be able to buy a home, let alone pay off the mortgage. In this book, you will discover our GLAD method that lets you pay off your mortgage in 10 years so you can retire mortgage-free. Owning your home free and clear is one of the best, most secure feeling of comfort you can imagine.

To achieve this, you’ll need to

pay off your mortgage faster.

Part 1

Intro

We will go into a broad overview of the steps that it takes in order to complete a flip from start to finish so you all can have a clearer idea of the process and the work involved in leading a successful flip.

Part 2

Marketing & Acquistion

Acquisition is one of the most important steps because if you don’t negotiate and purchase at the right price, you’ll end up shorting yourself and losing money.

Part 3

How & Where

to get $

The 3rd part in this series is about where to go and how to secure funding to make your flip project happen.

to get your free copy of

Calculating your DEBT SERVICE RATIO

PENALTY for breaking your mortgage

COST TO DO YOUR FLIP

CMHC changes will affect you

Effect March 17, 2017, CMHC rates are going up. Watch this brief video to learn about the changes and how this will affect you.

Investing in Rent-To-Own Property by Mark Loeffler **NEW ARTICLE**

I was never a fan of the Rent-To-Own strategy. Why would someone buy a house directly from me when they could go to the bank on their own? How do I prevent taking a potential loss by agreeing to sell the house to them without knowing the future worth of the house? For these and other reasons, I have never done a Rent-To-Own property. So when I came across “Investing in Rent-to-Own Property” by Mark Loeffler, my interest was peaked. I even went so far as buying my own copy of the book so I could highlight sections of interest to me.

This is a great book with very detailed steps on how to start and succeed with the Rent-To-Own strategy. What makes Mark’s strategy different is he gets the TENANT FIRST. As a real estate agent and investor, he has first-hand experience with this strategy. The book is written in an easy-to-read, non-boring format and very well organized showing two different qualifying families at different stages in their life. I read through the book twice and was interested both times on the twist he took.

The thing about this strategy is finding qualifying families that have the down payment. The book goes into detail about this, as this is critical in the TENANT FIRST Rent-To-Own strategy. Without this, the deal is a non-starter. The other factor that is crucial in this strategy is you, as the investor, will be assuming the mortgage and you must qualify for the mortgage.

A copy of this book can be purchased from: https://www.amazon.ca. Although the book was published in 2010, the content is still very relevant and the forms and examples provided are very helpful. Much of the content can also be applied to other real estate strategies (ie Credit reports, doing your due diligence, closing cost, etc.).

After reading the book twice, the Tenant-First-Rent-To-Own strategy is worth implementing. When the opportunity presents itself, I would not hesitate on offering this strategy. Although a visit to the website indicates Mark has not keep the site up to date since 2011, the book gets 2 thumbs up.

How to Find Positive Cash Flow Properties

This short video shows a very simple way to find cash positive properties. This technique can be used for any town or city in Canada. In this video we focus specially on Hamilton, Ontario.

Turn a Negative Cash Flowing Property Around

How do you turn a negative cash flowing property into a positive one? Here are a few suggestions.

- Look at increasing the monthly rent above the regulated guidelines. If you have a good relationship with your tenant, ask for a sit down. Explain the situation, show them documentation to support the increase in the heating cost, taxes, etc and ask if they are willing to increase the rental amount. Have a back up plan – which is to be prepared to file for a rent increase with the Landlord and Tenant Tribunal.

- Look at your expenses. Some small changes or payment reductions can make a cumulative big difference.

- Look at a rent-to-own option with your tenant. This only makes sense if your tenant has enough for a down payment and you are willing to sell the property in a few years. In this case, you have a tenant-first scenario.

Click on this link to get more suggestions and the rest of the story Reports

SUBCRIBE NOW!

Be the first to know when new videos are posted.

The information presented is from sources believed reliable, however, no responsibility is assumed for the accuracy of this information. The opinions or advice contained here should be verified with a third party. The content originator disclaims all responsibility and liability for the accuracy of the content.

Join our

NO MORE RENT

Program

Watch the video

Get the information

Fill out the application

Call us